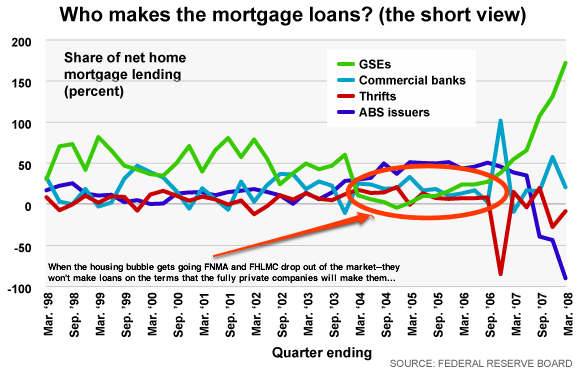

John McCain has been talking this bit of idiocy up ever since his call to fire the Chairman of the SEC landed like a dud. It has been taken up by the wingnut media for dissemination to their aggrieved and credulous constituencies. Let’s take a look at why this talking point is complete bull and why they think this is useful to them. This is going to be long (go get your cocktail now) — but unlike any wingnut talking point, there is plenty of data along the way here. We’ll start with this graph from Brad Delong:

Frankly, this ought to be the end of the discussion. Using data from the Federal Reserve Board, you can see who was writing mortgages throughout the life of the housing bubble though the bubble bursting. And the conforming mortgages that Fannie and Freddie could acquire became a smaller part of the total mortgage market share starting in 2002, absolutely cratered (for a combination of reasons — market, political, structural (their accounting scandal) in 2004, 2005 and started ramping back up as the bubble began to pop. The giant spike at the end is when the Administration (aided and abetted by Congress) rejiggered the conforming limits of these GSEs to get them to take on jumbo loans in an impotent attempt to put their fingers in the dike.

Fannie and Freddie have alot of problems (and have been repub targets for a long time — and not because of their problems, but that is another discussion) and as the housing markets get very hot, Fannie and Freddie acquired some bad habits in mortgage lending in trying to protect market share against the “innovative” ARMs that were being written at a fast pace. Fortunately for Fannie and Freddie, their charter restrictions keep them from acquiring too many toxic loans directly. Their charter restrictions didn’t keep them from investing fairly heavily into private label subprime and Alt-A securities, which is, of course, what has been blowing up.

The required reading of the issues of Fannie and Freddie comes from Calculated Risk in a post that responds to a July column of Paul Krugman’s, but provides the best unintentional rebuttal of the McCain talking point (and I encourage you to read the whole thing):

I think we can give Fannie and Freddie their due share of responsibility for the mess we’re in, while acknowledging that they were nowhere near the biggest culprits in the recent credit bubble. They may finance most of the home loans in America, but most of the home loans in America aren’t the problem; the problem is that very substantial slice of home loans that went outside the Fannie and Freddie box. But Krugman is right to focus on the fact that it was the regulatory and charter constraints of the GSEs that kept that box closed. In the schizoid reality of the GSEs, when they had their “shareholder-owned private company” hats on they did plenty of envelope-pushing. When they had their “affordable housing” hats on, they rationalized dubious theories of credit quality–like the fervent belief that low or no down payment can be fully offset by a pretty FICO score–to beef up their affordable housing goals, often at the expense not of the poor put-upon “private sector” but of FHA, whose traditional borrower pool they pretty thoroughly cherry-picked. Nonetheless, the immovable objects of the conforming loan limits and the charter limitation of taking only loans with a maximum LTV of 80% unless a well-capitalized mortgage insurer took the first loss position, plus all their other regulatory strictures, managed fairly well against the irresistible force of “innovation.” If there has ever been an argument for serious regulation of the mortgage markets, the GSEs are it.

Fannie and Freddie certainly followed the market into higher risk loans, but were stopped from going full-bore into the subprime paper business by their charter and conforming loan limits. They were allowed, by the Government, to keep less capital on hand to offset risk. And they were woefully under supervised by their government regulators. And they (acting like an investment fund) acquired lots of private label MBS’ backed by toxic mortgages. Sound like any other banks in the news recently? In addition, they were found to be overstating their capital in the last round of accounting scandals. And while everyone knew that Freddie and Fannie were drowning, Bush and the Congress decided to just pile on:

Congress and the administration both fell all over themselves to push the GSEs into jumbo markets they had at least managed to stay out of during the worst of the boom, cheerfully lifting their portfolio caps at the same time. How do you go on a stock-selling binge at the same time you have just become the official lender of last resort (along with FHA), handed the mandate to take out all those toxic ARMs with too-large loan balances into “safe” 30-year fixed that the borrowers in question still can’t afford?

With me so far?

The source of the claim that Fannie and Freddie were blown up by helping “poor people” may have come from their fired CEO, Richard Syron :the GSEs have been hit by a “100-year storm” in the housing market, accentuated by some higher-risk mortgages that they were forced to buy to meet government affordable-housing targets. But wrong. From the same Barron’s article:

The latter contention is more than disingenuous. A substantial portion of Fannie’s and Freddie’s credit losses comes from $337 billion and $237 billion, respectively, of Alt-A mortgages that the agencies imprudently bought or guaranteed in recent years to boost their market share. These are mortgages for which little or no attempt was made to verify the borrowers’ income or net worth. The principal balances were much higher than those of mortgages typically made to low-income borrowers. In short, Alt-A mortgages were a hallmark of real-estate speculation in the ex-urbs of Las Vegas or Los Angeles, not predatory lending to low-income folks in the inner cities.

Fannie and Freddie got caught by the many of the same issues that caught Lehman, Bear Stearns and the others queued up to fail — inadequate capitalization, lack of Federal oversight, mismanagement and a crashing housing market. Add to Fannie and Freddie’s story the mismanagement of funds and accounting fraud in an agency that helped launder overseas money into the US capital markets and you have an investment bank (it certainly acted like one) that the Fed made the case for bailing out.

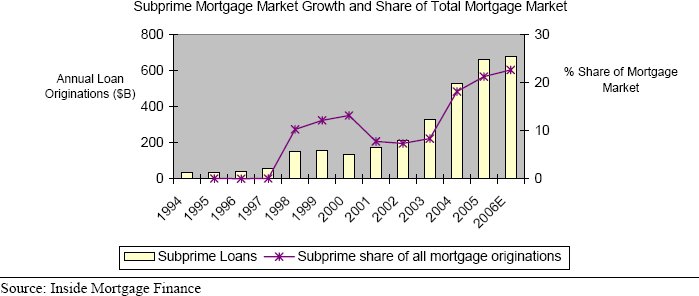

The bottom line here is that the repubs who have decided to push the notion that Fannie and Freddie are the culprit behind the meltdown are the financially ignorant of the wingnut class, speaking to the financially ignorant — expecting that their target audience will buy that somehow it is Democrats (see the grapgh above for the timeline) who wanted to get poor people into houses (which isn’t Fannie or Freddie’s mission) that is to blame for the current financial crisis. That, of course isn’t true, but Fannie and Freddie are special cases, for it is quite certain that both parties had been quite bought by Fannie and Freddie and both helped it to delay the inevitable. But take Fannie and Freddie off of the board and this meltdown still happens. Why? Look at this graph:

The proximate cause of the lock up of the credit markets is all of the mortgage-backed securities consisting of mostly the Alt-A and Subprime mortages that Fannie and Freddie (largely) couldn’t buy. Which is MOST OF IT. This bad paper was written for thoroughgoing middle class homeowners in fast growing places like California, Florida, Arizona, Nevada — mostly in major metro areas and rim suburbs. The majority of the “innovative” loans written for these houses weren’t conforming loans, so Fannie and Freddie aren’t even in the picture, except as a buyer of the ABSs that came from them. And so you know, foreclosures are going up at higher end homes including vacation homes, again — not Fannie or Freddie qualified.

That graph also tells us when the explosion of writing all of the bad paper exploded — certainly at a time when Democrats were not in charge of either the Executive or the Congress. At a time when this market needed someone watching over it and didn’t get it. Which doesn’t mean that Dems were not complicit in looking the other way as these bad mortgages marched towards their resets, but does certainly mean that they were not in the accountability seat as banks lost their minds and wrote all of this toxic paper, and once written, packed up and resold as investment securities.

The clumsy effort to blame Freddie and Fannie (while making pretend that IndyMac, Bear Stearns, Lehman, Merrill Lynch and all of the others queued up to fail don’t exist) for the banking meltdown does what our wingnut friends do best — lots of handwaving and contorted reasoning to avoid having the live with the consequences of their own malformed ideologies. And isn’t it interesting that they phone home to that old repub chestnut that “poor people” are somehow the root of all of our problems. For all of the chest puffery about a responsibility society not one of them will even consider the idea that the government did not force a single bank to write an obviously bad loan. There are no statutory requirements to write option ARMs, or to avoid (what used to be) the usual diligence in evaluating a borrower’s ability to pay or to waive downpayments or to use overheated appraisals or any of the other mortgage writing craziness that let these banks make money like no tomorrow for the past several years. And the authority that the Fed does have to reign in bank lending practices didn’t get used until this summer, and these new rules not only don’t go far enough, they don’t kick in until next year.

Many people looking for financing or refinancing of their homes (for whatever reason — acquiring investment properties to paying for medical bills or college tuition) were taken in by or willfully taking advantage of (or maybe both) the “innovative” mortgage business and poor people pay the larger price for its failures. It also creates a bigger space for predatory lenders to operate, especially since no one is minding the store. But every bad loan here has two parents — one who agreed to borrow more than he should have with crazy conditions that assumed your house was a cash register and the other who agreed to lend the money, while looking past all of the traditional red flags to the profits generated by this bad business. It’s just that the one who pretended that all loans were good loans gets to be made whole. And is the one excused by our wingnut friends.

The make-pretend world of repub free markets (And lets not pretend that Adam Smith has anything to do with this ideology’s world view) has been exposed for the sham that it is, exposed as one of the vectors for transferring money from taxpayers to this administration’s friends and the true believers (who don’t profit from being true believers other than venting their particularly delusional views of How The World Should Be) are reverting to form — ignorance about the institutions (and those institutions problems) they pretend to criticize, dishonesty about their own failed ideology, rewriting history and blaming “poor people” (and whoever that is supposed to be a proxy for) the failure of the policies that they actually advocated for as executed by BushCo.

(More reading if you are still here — A Business Week article from 2006 the sketches out the beginning of the toxic loan crisis and quaintly notes that the banks are protected from their excesses by the mortgage-basked securities they create to disperse the risk.)

Great post, Cass.

Wow.

How dare you try and confuse the situation with facts and fancy, elitist charts! It’s all Bill Clinton’s fault.

Seriously, impressive post.

Quick question – do your ‘wingnut friends’ live in your mirror?

Sorry…couldn’t resist.

outstanding post Cass.

I have one criticism.

Facts…you had way to many of them…

Pingback: Post Rescue - Meltdown 101 — Down With Absolutes!

Fannie Mae and Freddie Mac were co conspirators in this entire episode.

The other cohorts are Congress, The Executive Branch and of course the Banks.

Great post Cassandra!

I love these “Yeah, Yeah” responses…. There’s some real meat there guys. Yeah! Duh, no one implied they were solely responsible. You’re right, they are not. The Democrats push for everyone in a home regardless of their economic realities is more to blame. You can package it any way you want, but the general ideas are simply socialist and are wrong for America, just as health care is likely to end up Canadian quality if people don’t start using their intelligence and realize the Democratic party are not truly forward thinking and not only fail to see the big picture, but then missapropriate the “blame”.

For the record, Fannie and Freddie, while not “the cause” were certainly a part of the puzzle and Democrats openly resisted Republican-led efforts to regulate them further. Imagine that, requiring that people actually “qualify” for a loan might have saved us from this. This is not my personal “opinion”. You don’t have to be an elitist Harvard grad to understand this. You just have to be one to turn it around and blame the other party evidently.

Mitchell,

Don’t mistake “partly responsible” for “primarily responsible.” Republicans have controlled the White House for the past 8 years, 20 of the past 28 years, and have controlled Congress for 12 of the last 14, (and held enough seats in the last two years to uphold Bush vetos) but of course the mess we are in now is the Democrats fault. Republican propagandists truly have no shame. I love the citation to Republican efforts to regulate Fannie and Freddie. Those efforts occurred while the Republicans controlled Congress, but of course, its the Democrats fault. Most of the Republican claims are similarly laughable, if it weren’t that so many in our dumbed down soociety fall for them. One of my favorites is that because Fannie and Freddie bought up the better sub prime mortgage backed securities fromWall Street investment bankers, e.g. the Lehman Bros. of the world, it freed up more money for the private sector to invest in the really bad mortgages. That is the kind of “excuse” your mother woundn’t buy, “Fannie and Freddie made me do it.”

As for Canadian health care, try asking some Canadians how they like it, some will complain but the vast majority in poll after poll do not want to see a system like the US has, and why in the world would they want the most expensive system with one of the worst “outcomes” records of industrialized nations. I would think for the 47 million or so U.S. uninsured that George Bush said can just go to the emergency room would be damn glad to get “Canadian quality health care.” Don’t you think the Candians would have abandoned theirs if it was so bad.

You need to find a way to differentiate between propaganda and fact. You will see some distortion without question from the Democrats, but lets face, ever since the days of Lee Atwater’s dirty tricks brigade, through the “independent” Swift Boat ads, the Republicans have made it an art form; and after all, what else can they do, run on their real adgenda, “we want to take care of CEO’s and the top 1%, and the rest of you can go to hell.” They have to smear and propagandize to have any chance at all, and they get plenty of money for their top 1% patrons to run their appeals to the worst in all of us, selfishness, intoleance , and fear. Don’t worry though, as long as the Republicans keep appealling to the worst in human nature, they will always be able win some, if not most of the elections.

logic doesn’t work on republicans Rfk. accepting responsibility could be mean you are wrong. Being wrong is weak, and being weak is for liberals.